High NA EUV Lithography Process Market

High NA EUV Lithography Process Market is experiencing accelerated adoption as semiconductor manufacturers push toward sub‑13 nm patterning to meet the surging demand for AI‑centric, automotive, and high‑performance computing chips. Industry analysts project a sustained expansion through the 2026‑2034 forecast horizon, driven by major fab investments, emerging high‑NA tool generations, and an ecosystem of materials and metrology innovations.

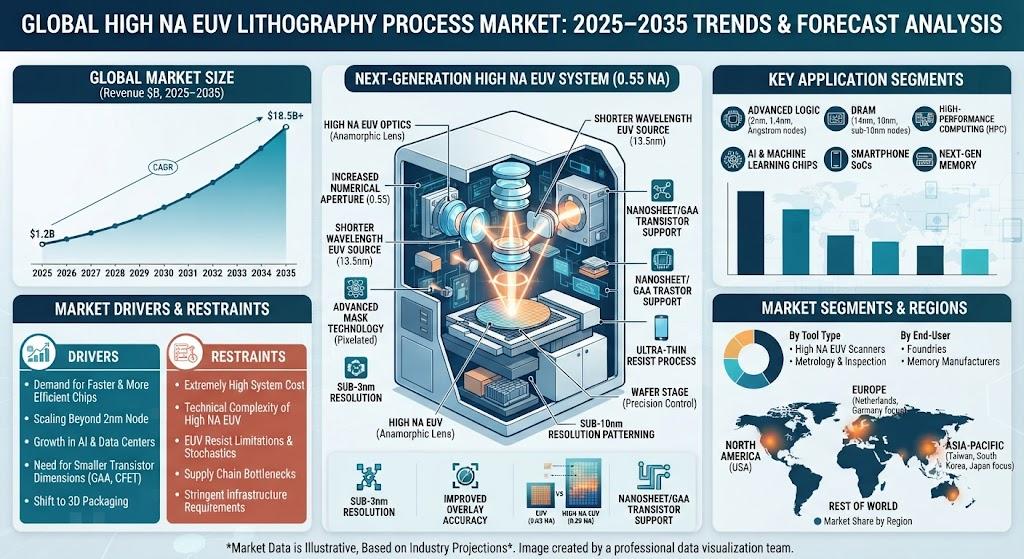

High NA EUV lithography, distinguished by its numerical aperture greater than 0.55, delivers the resolution improvements required for the next wave of logic and memory devices. The technology’s ability to print tighter pitches while maintaining high throughput is reshaping design rules and enabling new architectural possibilities across a broad range of semiconductor applications.

Download FREE Sample Report:

High NA EUV Lithography Process Market - View in Detailed Research Report

Key Growth Engines

The relentless scaling of transistor dimensions, coupled with the exponential growth of artificial‑intelligence workloads, has created an urgent need for lithographic solutions capable of sub‑10 nm patterning. Leading foundries such as TSMC, Samsung, and Intel have publicly announced multi‑billion‑dollar capital programmes that expressly allocate funds for high‑NA EUV equipment, wafer line upgrades, and the associated consumables ecosystem. In parallel, the development of high‑power laser sources, advanced pellicle technologies, and chemically amplified resists is shortening qualification cycles and reducing time‑to‑revenue for new nodes.

Strategic collaborations are further amplifying market momentum. The 2024 co‑development agreement between ASML and Intel, for example, aligns tool road‑maps with silicon design requirements, ensuring that high‑NA platforms can be seamlessly integrated into existing fab workflows. Government incentives in North America and Europe, focused on bolstering domestic semiconductor manufacturing, are also channeling additional funding toward high‑NA adoption, thereby diversifying the geographic footprint of the market.

Technology Landscape

High NA EUV lithography distinguishes itself through three core technological pillars:

-

Enhanced Optics: Larger numerical apertures (NA > 0.55) coupled with state‑of‑the‑art reflective mirrors deliver higher resolution and depth of focus.

-

Powerful Light Sources: High‑output laser systems, supplied primarily by Cymer and complemented by alternative providers such as Gigaphoton, enable the requisite photon flux for increased throughput.

-

Advanced Materials: Next‑generation photo‑resists, mask blanks, and pellicles are engineered to tolerate higher exposure energies while maintaining low line‑edge roughness.

These advancements are supported by a robust metrology and inspection infrastructure, with firms like KLA Corporation and Applied Materials providing the defect‑detection precision needed to sustain high yields on sub‑13 nm processes.

Market Segmentation Overview

The market can be dissected across several dimensions, each reflecting distinct strategic considerations for equipment manufacturers, material suppliers, and semiconductor fabs.

Segment Analysis:

COMPETITIVE LANDSCAPE

Key Industry Players

High NA EUV Lithography Process Market Competitive Landscape

ASML Holding NV remains the unequivocal market leader in high‑numerical‑aperture (NA > 0.55) EUV lithography, controlling an estimated 85 % of the equipment supply chain for the most advanced semiconductor nodes. The company's High‑NA EUV platform, slated for volume production in the early 2020s, delivers sub‑13 nm patterning capability that underpins the next wave of AI‑centric and automotive chips. Strategic collaborations-most notably the 2024 co‑development agreement with Intel-accelerate tool qualification and secure long‑term demand from leading fabs. ASML’s vertically integrated portfolio, which includes light‑source provider Cymer and optics specialist ZEISS, creates high barriers to entry and consolidates its dominant position across the entire high‑NA ecosystem.

Beyond ASML, a constellation of niche players contributes essential components and complementary technologies. Nikon and Canon, though focused on lower‑NA lithography, are investing in high‑NA research and may capture market share in specialized applications. Cymer supplies the high‑power laser sources critical for high‑NA throughput, while Gigaphoton offers alternative light‑source solutions for emerging fabs. Metrology and inspection firms such as KLA Corporation and Applied Materials provide precision defect detection and process control tools that enable the high yields required for sub‑13 nm production. Material suppliers including Lam Research and NeoPhotonics develop advanced photo‑resists and photonic components that optimize EUV exposure efficiency. Chipmakers themselves-Intel, Samsung Electronics, and Taiwan Semiconductor Manufacturing Co. (TSMC)-play a pivotal role by committing multi‑billion‑dollar fab investments, shaping the demand landscape and influencing supplier roadmaps.

List of Key High NA EUV Lithography Process Companies Profiled

-

ASML Holding NV

-

Intel Corporation

-

Samsung Electronics

-

Taiwan Semiconductor Manufacturing Co.

-

Nikon Corporation

-

Canon Inc.

-

Cymer

-

Gigaphoton Inc.

-

KLA Corporation

-

Applied Materials

-

Lam Research

-

NeoPhotonics

-

ZEISS (Optical Systems)

Segment Analysis:

|

Segment Category |

Sub-Segments |

Key Insights |

|

By Type |

|

Single‑Pattern High NA

|

|

By Application |

|

Logic Devices

|

|

By End User |

|

Foundries

|

|

By Technology |

|

Resist Development

|

|

By Market Driver |

|

AI Workloads

|

Get Full Report Here:

High NA EUV Lithography Process Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

Click here to Explore more-

https://semiconductorinsight.com/blog/tag/capacitive-linear-encoders-market-share/

https://semiconductorinsight.com/blog/tag/e-waste-disposal-market-trends/

https://semiconductorinsight.com/blog/tag/ic-substrate-micro-drill-market-2025/

https://semiconductorinsight.com/blog/tag/e-waste-disposal-market-size/

https://semiconductorinsight.com/blog/tag/chemical-vapor-deposition-cvd-market-growth/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us