Semiconductor Equipment for Advanced Packaging Market

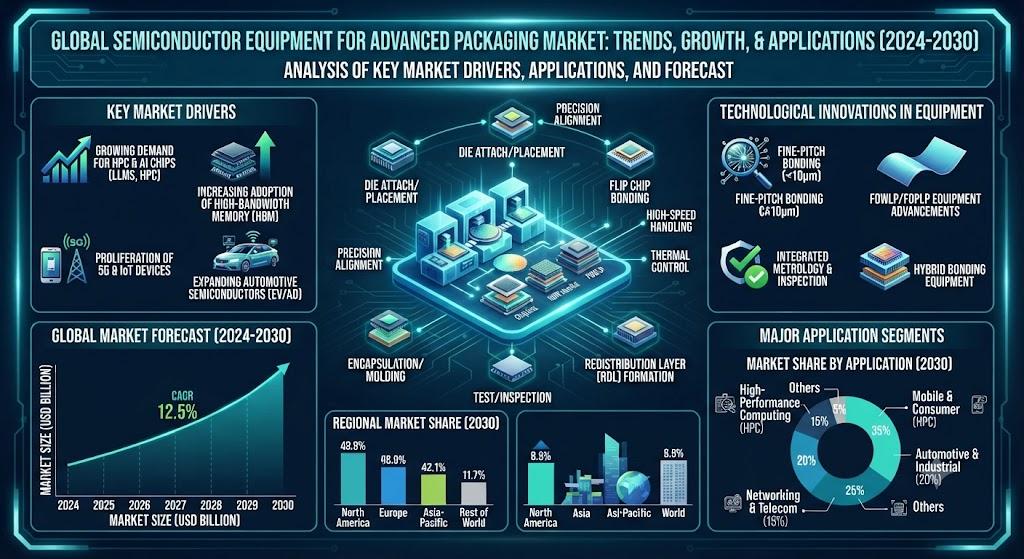

Semiconductor Equipment for Advanced Packaging Market, valued at a robust USD 14.8 billion in 2025, is on a clear trajectory of expansion, propelled by the explosive demand for heterogeneous integration, AI‑centric workloads, and high‑performance computing. This growth narrative is captured in a comprehensive new study released by Semiconductor Insight, which examines how next‑generation packaging tools are reshaping the semiconductor value chain and enabling chip architectures that were once considered aspirational.

Advanced packaging equipment-including wafer‑level fan‑out (FOWLP) platforms, chip‑on‑wafer (CoW) integration tools, and precision die‑attach systems-has become a cornerstone of modern semiconductor manufacturing. These tools empower foundries and IDMs to push interconnect density, reduce signal latency, and achieve power efficiencies that meet the stringent requirements of emerging applications such as autonomous vehicles, edge AI, and 5G infrastructure.

Download FREE Sample Report:

Semiconductor Equipment for Advanced Packaging Market - View in Detailed Research Report

Semiconductor Industry Expansion: The Primary Growth Engine

The report identifies the rapid evolution of the semiconductor industry as the single most influential driver for advanced‑packaging equipment demand. With AI accelerators, high‑bandwidth memory, and 3‑D‑stacked solutions commanding a larger share of silicon revenue, the need for tooling that can reliably stack, bond, and test multi‑die ensembles is accelerating. The broader semiconductor equipment market, already exceeding $120 billion annually, supplies a fertile ecosystem where advanced packaging solutions represent a fast‑growing sub‑segment.

“The concentration of leading‑edge fabs and equipment manufacturers in the Asia‑Pacific region-home to more than three‑quarters of global wafer capacity-creates a powerful catalyst for advanced packaging equipment adoption,” the report notes. Governmental investments surpassing $500 billion through 2030, combined with strategic initiatives to localize supply chains, further intensify the demand for sophisticated packaging platforms that can handle sub‑micron alignment and ultra‑thin die‑thickness.

Read Full Report: https://semiconductorinsight.com/report/semiconductor-equipment-advanced-packaging-market/

Market Segmentation: Advanced Fan‑Out, Chip‑On‑Wafer and 3‑D Integration Lead

The study provides a granular segmentation analysis that outlines the market’s structural composition and highlights the segments poised for the strongest growth:

Segment Analysis:

By Type

-

Wafer‑level fan‑out (FOWLP) platforms

-

Chip‑on‑wafer (CoW) integration tools

-

Other niche integration technologies

By Application

-

High‑performance computing (HPC) modules

-

AI accelerator packages

-

Mobile and consumer electronics

-

Automotive and industrial control

-

Others

By End User

-

Foundries

-

OEMs / ODMs

-

Integrated device manufacturers (IDMs)

By Technology

-

Next‑generation lithography for fan‑out

-

High‑precision die‑attach bonding

-

In‑situ inspection and metrology

By Process Stage

-

Pre‑bond preparation

-

Bonding & interconnect formation

-

Post‑bond inspection & testing

Segment Analysis:

|

Segment Category |

Sub-Segments |

Key Insights |

|

By Type |

|

Advanced Fan‑Out Solutions dominate because they enable fine‑pitch interconnects and high‑density routing without increasing form factor.

|

|

By Application |

|

AI Accelerator Packages dominate this dimension as designers increasingly rely on multi‑chip stacking to meet AI model complexity.

|

|

By End User |

|

Leading Foundries are the primary end‑users because they drive volume production and standardize advanced packaging processes.

|

|

By Technology |

|

Next‑Generation Lithography is perceived as the most transformative technology, enabling finer line widths and tighter pitch.

|

|

By Process Stage |

|

Bonding & Interconnect Formation commands attention because it directly influences electrical performance and mechanical reliability.

|

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Equipment for Advanced Packaging – Competitive Landscape Overview

The advanced packaging segment of the semiconductor equipment market is dominated by a handful of global innovators that together account for more than half of the 2025 market value of USD 14.8 billion. Applied Materials leads with its next‑generation fan‑out lithography platform, leveraging deep R&D investment to capture high‑growth AI and HPC demand. ASML supplies extreme‑ultraviolet (EUV) and next‑generation lithography tools essential for wafer‑level fan‑out (FOWLP) processes, while Lam Research and Tokyo Electron provide critical deposition, etch, and cleaning equipment that underpin heterogeneous integration. KLA Corporation complements the ecosystem with high‑precision inspection and metrology solutions that ensure yield in three‑dimensional stacking. The collective emphasis on scalability, throughput, and cost‑of‑ownership shapes a market structure where tier‑one vendors drive technology roadmaps and secure long‑term supply contracts with major foundries.

Beyond the tier‑one cohort, a diverse set of niche specialists expands the functional breadth of the advanced packaging supply chain. SCREEN Holdings offers wafer‑level bonding and polymer deposition systems that are particularly valuable for fan‑out wafer‑level packaging. Canon Tokki remains a leader in organic light‑emitting diode (OLED) and die‑attach equipment, supporting emerging chip‑on‑wafer (CoW) applications. Advantest and Teradyne provide test and measurement platforms that validate multi‑chip modules, while Hitachi High‑Technologies and Nordson supply precision die‑attach and dispensing tools for heterogeneous integration. Regional players such as SUSS MicroTec contribute advanced lithography and wafer‑handling technologies, reinforcing a competitive landscape that blends large‑scale innovation with highly specialized capabilities.

List of Key Semiconductor Equipment for Advanced Packaging Companies Profiled

-

Applied Materials

-

ASML Holding

-

Lam Research

-

Tokyo Electron

-

KLA Corporation

-

SCREEN Holdings

-

Canon Tokki

-

Advantest

-

Teradyne

-

Hitachi High‑Technologies

-

Nordson

-

SUSS MicroTec

These companies are focusing on technological advancements such as integrating IoT for predictive maintenance, expanding tool automation, and securing geographic expansion into high‑growth regions like Asia‑Pacific to capitalize on emerging opportunities.

Emerging Opportunities in Emerging Verticals

Beyond the traditional telecom and consumer electronics drivers, the report outlines significant opportunities in electric‑vehicle (EV) battery pack manufacturing, renewable energy inverter production, and aerospace avionics. All of these sectors demand high‑density interconnects, strict thermal budgets, and reliability standards that advanced packaging equipment can deliver. Moreover, the convergence of Industry 4.0 principles with packaging tools-through AI‑enabled process control and real‑time metrology-promises to reduce unplanned downtime and enhance yield predictability.

Report Scope and Availability

The market research report delivers a holistic analysis of the global and regional Semiconductor Equipment for Advanced Packaging markets from 2025–2034. It includes detailed segmentation, market size forecasts, competitive intelligence, technology trend assessments, and an evaluation of key market dynamics shaping the ecosystem.

Get Full Report Here:

Semiconductor Equipment for Advanced Packaging Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

Click here to Exlpore more-

https://semiconductorinsight.com/report/pin-photo-diode-market/embed/

https://semiconductorinsight.com/report/fc-fibre-channel-interface-tape-library-market/embed/

https://semiconductorinsight.com/report/global-leaded-disk-varistor-market/embed/

https://semiconductorinsight.com/report/radiation-detection-market/embed/

https://semiconductorinsight.com/report/global-contact-level-sensors-market/embed/

https://semiconductorinsight.com/report/global-rf-surge-suppressors-market/embed/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us