Smart Agriculture Solution Market to Reach USD 34.6 Billion by 2036 as Precision Farming and IoT Automation Drive 6.9% CAGR

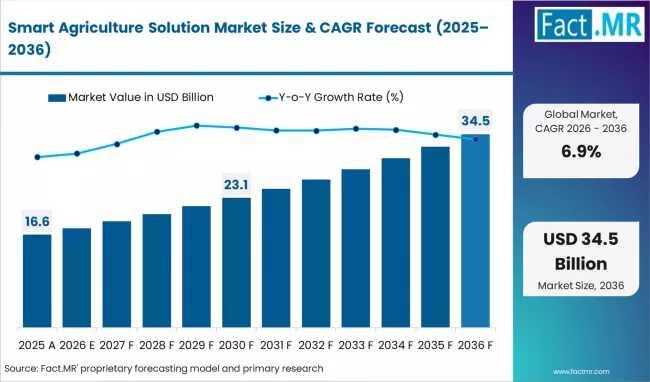

Global agricultural industries and food production systems are experiencing a fundamental structural transition as agribusiness heads, plantation managers, and cultivation leads shift away from traditional, manual farming methodologies toward integrated, data-driven precision technology. According to an extensive new market evaluation published by Fact.MR, the global smart agriculture solution market is projected to grow from an industry valuation of USD 17.7 billion in 2026 to an absolute market valuation of USD 34.6 billion by 2036.

Get detailed market forecasts, competitive benchmarking, and pricing trends:

This trajectory represents a compound annual growth rate (CAGR) of 6.9% over the ten-year forecast horizon, presenting a massive absolute dollar opportunity for agricultural machinery manufacturers, IoT sensor developers, and agronomic software innovators.

Key Market Highlights at a Glance

- Estimated Market Size in 2026 (Base Year): USD 17.7 billion

- Projected Market Size by 2036 (Forecast Year): USD 34.6 billion

- Compound Annual Growth Rate (CAGR): 6.9% between 2026 and 2036

- Dominant Component Segment: Hardware capturing approximately a 45% market share in 2026

- Leading Application Segment: Automated Machinery Guidance Control representing a 30% market share in 2026

- Core Hardware Offerings: Sensor Monitoring Systems, Smart Detection, GPS-Enabled Ranging, and Ag-Drones

- Core Service Offerings: Climate Information, Supply Chain Management, System Integration, and Maintenance

- High-Growth National Market: United States expanding at an 11.5% CAGR through 2036

- Competitive Structure: Moderately fragmented value chain comprising major OEMs, precision tech specialists, and agronomic data platforms

Why Is the Smart Agriculture Solution Market Growing?

- Aggressive Adoption of Precision Agriculture: Farming enterprises are rapidly installing real-time field monitoring equipment to optimize seed placement, fertilizer application, and crop spraying.

- Escalating Labor Scarcity and Operational Costs: The ongoing shortage of manual field labor globally is forcing large-scale commercial farms to deploy automated machinery and drone systems to maintain high yields.

- Integration of Next-Gen IoT and Climate Services: Modern producers are relying heavily on hyper-local climate information services and connected sensor arrays to insulate crop yields from unpredictable weather volatility.

"The global agricultural sector is moving well beyond reactive, legacy crop management," states an industry analyst at Fact.MR. "Enterprise growers and food producers require continuous, predictive field intelligence. Industry adoption is shifting rapidly toward integrated digital platforms that connect heavy physical machinery with real-time sensor networks to maximize input efficiency."

Which Component Leads the Smart Agriculture Solution Market Share?

The operational backbone of data-driven cultivation relies on physical data capture points and field-level mechanisms. The hardware segment is projected to account for around 45% share of the smart agriculture solution market by 2026. This leading position is driven by the immediate requirement for robust physical hardware—including soil sensors, field cameras, GPS-enabled ranging components, and specialized agricultural drones—to capture baseline field analytics. As digital platforms advance, the physical hardware layer remains the essential primary investment required to feed algorithms actionable farm metrics.

- Hardware Component Market Share: ~45% of the global marketplace in 2026

- Core Functional Focus: Real-time agricultural data collection regarding soil chemistry, moisture levels, crop growth, and machinery performance

- Market Integration Value: Serves as the localized data ingest infrastructure, feeding remote cloud-analytics platforms and automation software

Which Application Axis Commands Major Industry Volume?

Optimizing field execution patterns and maximizing raw acreage utilization represents the fastest-adopted commercial application for digital farming tools. The automated machinery guidance control segment is expected to represent approximately a 30% share of the smart agriculture solution market in 2026. This major market share is sustained by the heavy deployment of GPS and sensor-based systems that auto-steer tractors, sprayers, and harvesters. These automated systems eliminate overlapping passes, minimize fuel wastage, and maintain strict row accuracy during planting and crop protection operations.

- Automated Machinery Guidance Control Share: ~30% of application demand in 2026

- Volume Catalyst: Commercial farms deploying self-guided equipment networks to combat rising fuel expenses and operator fatigue

- Operational Focus: Standardizing tractor paths to protect crop rows and optimize raw input distribution without manual tracking errors

Market Dynamics

Core Market Drivers

The primary driver accelerating global industry expansion is the urgent commercial necessity to maximize global crop yields while minimizing chemical and water inputs. Additionally, precision agriculture initiatives backed by international food security departments and tech rollouts by industry heavyweights like John Deere are encouraging mass enterprise procurement of smart equipment networks.

Primary Market Restraints

The primary restraint limiting faster global adoption is the high initial capital expenditure required to outfit existing fleet machinery with advanced satellite receivers and predictive analytics networks. For medium-to-small farming operations, this heavy upfront investment combined with a steep technical learning curve often slows down the initial technology deployment cycle.

Prominent Industry Trends

The most significant trend defining the current landscape is the convergence of heavy agricultural machinery with cloud-connected artificial intelligence. Drone platforms are shifting from basic aerial photography toward automated localized spraying systems. Concurrently, manufacturers are integrating real-time computer vision into row sprayers to spot-treat weeds on an individual basis, significantly cutting herbicide volume.

Regional Outlook: Precision Infrastructure Mandates Fuel Explosive Growth in the United States

The systemic requirement to secure grain supply chains and increase per-acre throughput is generating distinctive growth curves across major global breadbaskets.

- United States Forecasted Growth Rate: 11.5% CAGR from 2026 to 2036

- Key Regional Geographies Analyzed: North America, Western Europe, East Asia, and Emerging Agriculture Hubs

The United States is projected to rise at an 11.5% CAGR through 2036, leading the global marketplace in precision technology investment velocity. This growth is heavily supported by precision agriculture initiatives promoted by the United States Department of Agriculture (USDA) and the continuous expansion of digital farming systems across the Midwest corn and soybean belts.

Western Europe follows closely with intense demand centered around smart detection systems and automated irrigation controllers, catalyzed by strict regional mandates on synthetic fertilizer reductions and water preservation. In East Asia, development is largely driven by automated drone technologies and climate services optimized for high-density terraced farming and regional specialty crops.

Competitive Landscape: Strategic Focus on Connected Software Ecosystems and Equipment Integration

The competitive landscape of the smart agriculture solution market is moderately fragmented, featuring a mix of legacy industrial machinery manufacturers, standalone precision tech providers, and agronomic data startups.

- John Deere (Deere & Company): Continues to expand its unified digital ecosystem, delivering factory-integrated autonomous tractor options and deep data-analytics platforms.

- Trimble Inc.: Focuses on advanced GPS ranging systems, guidance displays, and third-party hardware integration tools for mixed-brand fleets.

- Topcon Positioning Systems: Specializes in precision auto-steering solutions, variable-rate control hardware, and smart sensor modules.

- Raven Industries (CNH Industrial): Prioritizes high-speed field application control systems and autonomous agricultural technology systems.

Competitive dynamics show that selling siloed hardware components is no longer sufficient to secure a premium market position. Leading technology brands are heavily prioritizing cross-platform software integration, robust API connections for third-party agronomic tools, and specialized maintenance and consulting services to provide a seamless, plug-and-play user experience for modern agribusinesses.

Frequently Asked Questions

What is the projected global value of the smart agriculture solution market by 2036?

The global smart agriculture solution market is projected to reach an absolute market valuation of USD 34.6 billion by the year 2036.

What is the expected compound annual growth rate of the smart agriculture technology sector?

The market is expected to expand at a compound annual growth rate (CAGR) of 6.9% from 2026 to 2036.

Which component type holds the highest market share within the smart agriculture market?

The hardware component segment—including sensors, drones, and GPS-enabled ranging tools—leads the market, capturing roughly a 45% share in 2026.

What application segment commands the largest share of the smart farming solutions industry?

Automated machinery guidance control systems dominate the application axis, representing approximately a 30% share of the global marketplace in 2026.

At what rate is the United States smart agriculture solution market projected to expand?

Demand within the United States is projected to rise at a rapid compound annual growth rate (CAGR) of 11.5% through 2036.

Who are the prominent hardware and platform vendors operating within this industry?

Key market participants include John Deere, Trimble Inc., Topcon Positioning Systems, and Raven Industries.

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com