Automotive Brake Friction Products Market Share and Forecast, Accelerating to US$ 23.24 Billion by 2034, 4.34% CAGR

Every time you press down on your car's brake pedal, a highly orchestrated sequence of physics and material science takes place. Kinetic energy is transformed into thermal energy, safely bringing several thousand pounds of steel to a smooth, predictable halt. At the absolute heart of this critical safety sequence are brake friction products the unsung heroes of automotive safety, including brake pads, shoes, linings, and discs.

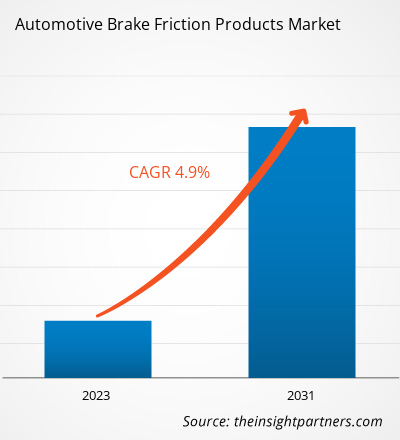

As global vehicle production shifts gears toward electrification and automated safety systems, the components keeping us safe are undergoing a quiet revolution. According to a comprehensive research study by The Insight Partners, the financial footprint of this industry is expanding significantly. The Automotive Brake Friction Products Market size is expected to reach US$ 23.24 Billion by 2034 from US$ 15.86 Billion in 2025. The market is anticipated to register a CAGR of 4.34% during the forecast period 2026–2034.

This steady trajectory reflects an evolving transportation landscape where safety mandates, vehicle architecture changes, and consumer driving environments are collectively redefining the friction materials we rely on.

What is Driving the Need for Friction Materials?

The demand for high-end automotive brake friction components boils down to two main avenues: original equipment manufacturing (OEM) installations for new cars and the continuous aftermarket replacement loop.

1. The Growing Stress of Urban Congestion

One of the most persistent, everyday drivers behind the expansion of the aftermarket sector is rising traffic congestion. In ever-expanding urban centers, typical daily commutes involve a ceaseless rhythm of stop-and-go driving. This continuous, repetitive application of the brakes introduces intense thermal stress and mechanical abrasion to brake pads and shoes. Over time, friction power degrades, creating a non-negotiable need for routine replacement parts to maintain vehicle safety and optimal stopping distance.

2. Rising Vehicle Production and Global Fleets

Even as mobility concepts evolve, global automotive manufacturing continues to scale up to keep pace with growing middle-class populations in emerging economies specifically across the Asia-Pacific region. Increased passenger car sales and growing logistics fleets necessitate a massive volume of factory-installed brake components annually.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00028378

Material Innovation: Ceramic, Metallic, and Beyond

Manufacturers are no longer just pressing basic organic components together. Modern automotive dynamics demand brake friction materials customized to distinct vehicle classes and performance criteria:

-

Metallic and Semi-Metallic:Exceptionally durable and offering excellent heat dissipation, metallic compounds remain highly favored in heavy commercial vehicles (HCVs) and high-performance racing platforms where stopping power under intense stress is critical.

-

Ceramic:Gaining substantial ground in the premium passenger car segment, ceramic formulations offer an incredibly quiet ride, lower dust production, and decreased rotor wear, directly answering consumer demands for better Noise, Vibration, and Harshness (NVH) characteristics.

-

Composites and Eco-Friendly Alternatives: Strict environmental regulations, such as the global push to eliminate copper and heavy metals from brake formulations (which pollute waterways via road runoff), have forced intense R&D into non-asbestos organic (NAO) materials and advanced phenolic composites.

The Competitive Landscape

The global brake friction space is characterized by a balance of established tier-1 suppliers and specialized aftermarket manufacturers focusing on rapid technological deployment. Key players shaping the present and future of this industry include:

-

ABS Friction

-

Akebono Brake Industry Co., Ltd.

-

Bendix Spicer Foundation Brake, LLC

-

Bosch Limited

-

Carlisle Brake & Friction, Inc.

-

Delphi Auto Parts

-

Japan Brake Industrial Co., Ltd.

-

Aisin Corporation

-

Miba AG

-

Nisshinbo Brake Inc.

These industry leaders are actively establishing local manufacturing footprint expansions, securing exclusive OEM contracts, and rolling out specialized product lines tailored specifically to the unique wear cycles of next-generation powertrains.

Future Outlook

Looking ahead, the automotive brake friction products market will be profoundly shaped by the rapid dual forces of vehicle lightweighting and powertrain electrification.While electric and hybrid vehicles rely extensively on regenerative braking a technology where the electric motor handles a massive portion of initial deceleration physical friction brakes remain an absolute fail-safe for emergency stops and low-speed parking dynamics.This shift is steering the industry away from traditional, high-volume replacement cycles and moving it toward specialized, high-margin materials.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com