Global Airborne Radars Market Outlook Post 2025: Reaching US$ 20.68 Billion by 2034 at 7.52% CAGR

The landscape of global aerospace and defense electronics is undergoing a major evolution, driven by the escalating demand for high-fidelity situational awareness, multi-domain military operations, and reliable commercial aviation safety tools. At the center of this technological paradigm shift lies the airborne radar system. Deployed across multi-role fighter jets, unmanned aerial vehicles (UAVs), maritime patrol planes, and civilian aircraft, modern airborne radars are transitioning from standard hardware sensors to highly adaptive, software-defined data hubs. This article provides a comprehensive overview of the market dynamics, prominent industry participants, and upcoming trends shaping this sector.

Market Size and Growth Trajectory

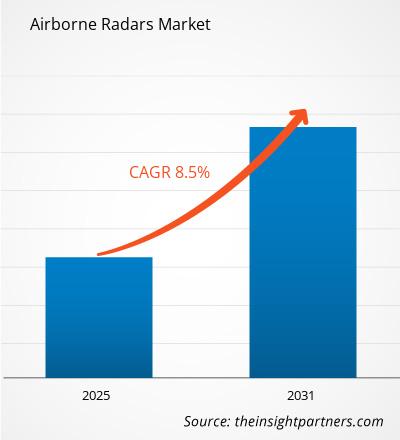

The global airborne radars market is experiencing a period of robust capital deployment and strategic scaling. According to data published by The Insight Partners, the Airborne Radars Market size is expected to reach US$ 20.68 Billion by 2034 from US$ 11.58 Billion in 2025. This expansion represents a steady development curve, with the market estimated to record a CAGR of 7.52% from 2026 to 2034.

This strong growth is primarily fueled by accelerated military modernization frameworks worldwide. Many nations are phasing out outdated mechanical radar arrays in favor of sophisticated digital radar variants. The persistent rise in regional geopolitical disputes has forced global defense departments to prioritize early-warning security networks, deep-target acquisition, and sovereign airspace policing capabilities. Consequently, defense acquisition budgets are heavily leaning toward long-term contracts for advanced airborne reconnaissance assets.

Crucial Drivers Accelerating Market Adoption

Several systemic forces underpin the ongoing expansion of the airborne radar industry:

-

The Proliferation of Unmanned Aerial Vehicles (UAVs): The integration of mini-radars into tactical and high-altitude long-endurance (HALE) drones has transformed remote intelligence gathering. Modern security frameworks demand lightweight, low-SWaP (Size, Weight, and Power) radar payloads that can deliver high-resolution mapping without compromising drone flight endurance.

-

Transition to Active Electronically Scanned Array (AESA) Tech: AESA systems have emerged as the absolute benchmark for modern combat platforms. Unlike historical mechanical systems, AESA modules utilize hundreds of micro-transmit/receive elements capable of steering radio beams electronically. This ensures rapid target scanning, vastly improved tracking limits, and multi-mission capabilities allowing simultaneous mapping and electronic warfare defense.

-

Upgrades to Civilian and Commercial Fleet Logistics: Beyond national defense boundaries, civil aviation organizations and global commercial carriers continue to invest in state-of-the-art airborne weather radars and advanced terrain-avoidance software. Driven by structural air-traffic management overhauls, these retrofits bolster flight optimization paths, shield aircraft from extreme meteorological hazards, and drastically lower mid-air collision probabilities.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022710

Major Competitors and Industry Leaders

The competitive ecosystem is characterized by a mix of established tier-one aerospace giants and agile electronic systems providers that consistently push the boundaries of radio frequency (RF) semiconductor engineering.

The key players operating within the global market include:

-

Lockheed Martin Corporation – A premier market force delivering multi-mode radar integrations for international 5G-enabled strike fighter programs like the F-35 Lightning II.

-

Northrop Grumman Corporation – Widely recognized for pioneering scalable agile beam radar technologies and providing dominant long-range fire control airborne platforms.

-

Thales Group – A European aviation leader offering cutting-edge RBE2 AESA arrays for multi-role fighters and comprehensive commercial aviation safety components.

-

Hensoldt AG – A major developer of modular, multi-mission sensor arrays tailored for tactical military transport, early-warning platforms, and rotary aircraft.

-

Leonardo SPA – An engineering pioneer focusing on high-performing mechanical and digital scanning surveillance radars optimized for maritime safety and border patrol fleets.

-

BAE Systems – Provides deeply integrated electronic combat suites and high-durability radar components engineered to withstand contested electronic-jamming spaces.

-

Israel Aerospace Industries (IAI) – Renowned through its Elta division for executing high-end airborne early warning and control (AEW&C) radar system rollouts.

-

Saab AB – Offers exceptional early warning radar configurations, including the highly regarded Erieye multi-role sensor package for long-range threat mapping.

-

Aselsan – A rising regional giant executing significant defense localization projects and engineering domestic multi-mode fire control radars.

-

Elbit Systems – Specializes in developing cutting-edge, compact radar modules perfectly tailored for complex UAV flight patterns and targeted search-and-rescue systems.

Future Outlook

Looking toward the horizon, the airborne radars market is poised to transition from purely hardware-focused setups to highly integrated cognitive architectures. The incorporation of Artificial Intelligence (AI) and Machine Learning (ML) into signal processing frameworks stands out as a defining trend for the upcoming decade. Next-generation cognitive radar systems will possess the intelligence to automatically adapt their waveforms and frequency ranges in real time, neutralizing complex electronic jamming from adversaries in contested electromagnetic spaces.

Furthermore, the rapid commercialization and adoption of Gallium Nitride (GaN) semiconductor chemistry will continue to replace older Gallium Arsenide (GaAs) components. This material shift allows airborne radars to transmit significantly higher power outputs while reducing physical weight footprints and thermal management overhead. As multi-domain combat operations become the default strategy for global military planners, airborne radars will increasingly function as nodes within unified mesh networks seamlessly collecting, analyzing, and distributing battlefield data across naval forces, ground centers, and space assets.

Related Reports-

Airborne Weapon Delivery Systems Market

Airborne ISR as a Service Market

Airborne Persistent Surveillance System Market

Airborne Collision Avoidance System Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com