Global Silver Tungsten Electrodes Market to Reach USD 487.2 Million by 2034 as Electronics, EDM, and EV Applications Drive Demand

Silver Tungsten electrodes are advanced composite materials designed to perform under extreme electrical, thermal, and mechanical stress. These electrodes combine the high electrical and thermal conductivity of silver with the hardness, high melting point, and arc erosion resistance of tungsten, creating a material system that is highly valued in precision industrial applications.

Unlike conventional electrode materials, Silver Tungsten electrodes are engineered for situations where durability, conductivity, dimensional stability, and resistance to wear are all required at the same time. Their composition typically contains 20% to 50% silver by weight, depending on the desired balance between conductivity and erosion resistance.

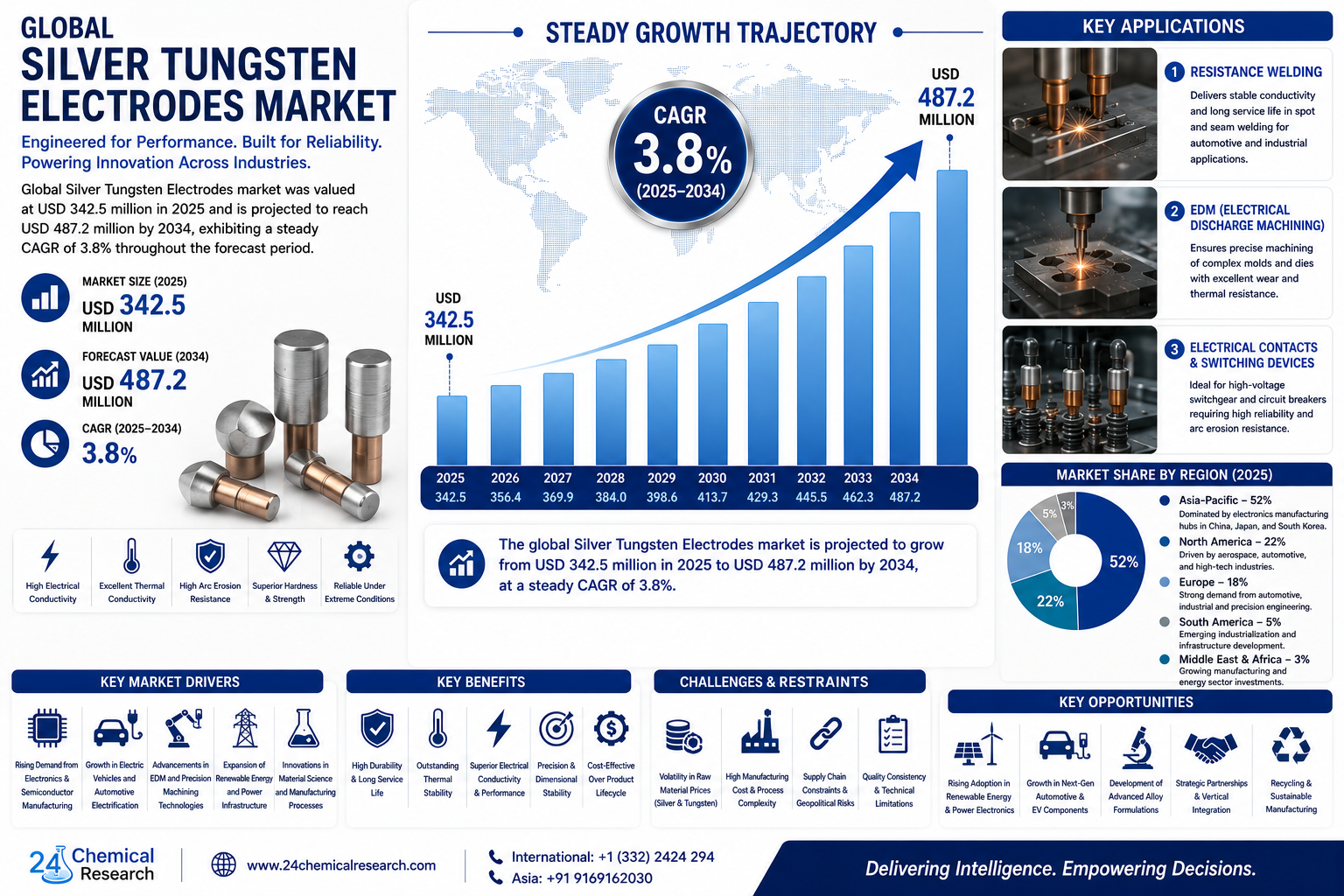

Global Silver Tungsten Electrodes market was valued at USD 342.5 million in 2025 and is projected to reach USD 487.2 million by 2034, exhibiting a steady CAGR of 3.8% throughout the forecast period. Demand is being supported by electronics manufacturing, semiconductor tooling, electrical discharge machining, resistance welding, high-voltage switching devices, electric vehicles, aerospace systems, and renewable energy infrastructure.

Get Full Report Here:

https://www.24chemicalresearch.com/reports/307186/silver-tungsten-electrodes-market

Market Dynamics:

The trajectory of the Silver Tungsten Electrodes market is governed by a dynamic interplay of powerful growth drivers, significant adoption restraints, technical challenges, and expanding opportunities across high-precision manufacturing and advanced electrical systems. While the growth of electronics, automotive electrification, and renewable energy infrastructure supports demand, manufacturers must also manage raw material price volatility, production complexity, and quality consistency requirements.

Key Market Highlights

● Global Silver Tungsten Electrodes market was valued at USD 342.5 million in 2025 and is projected to reach USD 487.2 million by 2034.

● The market is expected to grow at a steady CAGR of 3.8% throughout the forecast period.

● Silver Tungsten electrodes are widely used in resistance welding, electrical discharge machining, and electrical contacts for switching devices.

● Electronics and semiconductor manufacturing account for the largest share of demand due to precision machining and micro-component assembly requirements.

● Automotive electrification is creating new demand for high-power relays, contactors, and battery management systems.

● Asia-Pacific dominates global consumption, supported by electronics manufacturing, semiconductor production, and strong industrial supply chains.

● Renewable energy infrastructure, next-generation alloys, and strategic OEM partnerships represent major future growth opportunities.

Powerful Market Drivers Propelling Expansion

-

Surging Demand from Electronics and Semiconductor Manufacturing:

The electronics and semiconductor industries represent one of the most important growth drivers for the Silver Tungsten Electrodes market. As electronic devices become smaller, more complex, and more performance-intensive, manufacturers require precision tooling and electrode materials that can maintain stability under demanding operating conditions.

Silver Tungsten electrodes are used in precision welding for micro-component assembly and in electrical discharge machining processes for producing complex molds, dies, and components used in semiconductor manufacturing. Their resistance to wear and ability to maintain dimensional accuracy make them valuable in high-precision operations.

The global electronics market exceeds $1.5 trillion, and the continuous rise of smartphones, consumer devices, sensors, microchips, circuit components, and advanced electronic modules supports consistent demand for specialized manufacturing materials. Silver Tungsten electrodes are especially useful where ordinary electrode materials may deform, erode, or lose performance under high thermal and electrical loads.

Asia-Pacific manufacturing hubs, particularly China, Japan, South Korea, Taiwan, and Southeast Asian electronics clusters, are key demand centers. As semiconductor fabrication and electronics assembly continue expanding, the need for high-quality electrode materials is expected to remain strong.

-

Accelerated Automotive Electrification:

The global transition toward electric vehicles is creating a major growth opportunity for Silver Tungsten electrodes. Electric vehicles require reliable electrical components capable of handling frequent high-current switching, thermal stress, and long service life requirements.

Silver Tungsten materials are used in high-power relays, contactors, battery management systems, charging systems, and electrical switching devices. These components must withstand repeated electrical arcs and maintain stable conductivity without excessive degradation.

With annual global EV sales projected to surpass 30 million units by 2030, demand for durable electrical contact materials is increasing rapidly. EV powertrains, battery packs, charging infrastructure, and power electronics require materials that can perform reliably under high load conditions.

Silver Tungsten alloys are well suited to this environment because they combine silver’s conductivity with tungsten’s arc resistance and mechanical durability. This makes them important for the automotive industry’s shift toward electrified platforms, higher voltage architectures, and advanced power control systems.

-

Advancements in Material Science and Manufacturing:

Ongoing innovation in powder metallurgy, sintering processes, and composite material engineering is improving the performance and commercial viability of Silver Tungsten electrodes. These advances allow manufacturers to create more uniform microstructures, better silver distribution, and improved electrode consistency.

More homogeneous material structures can improve conductivity, reduce localized wear, and extend operating life. In some cases, improved manufacturing techniques can increase electrode lifespan by 15-20%, supporting better cost performance for industrial users.

Advanced production methods also allow manufacturers to tailor electrode properties for specific applications. For example, different silver-tungsten ratios can be optimized for EDM, resistance welding, circuit breakers, relays, aerospace systems, or renewable energy equipment.

These improvements are expanding the application scope of Silver Tungsten electrodes. As industries require materials that can handle higher power density, smaller component geometry, and longer operating cycles, advanced composite electrodes are becoming increasingly important.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307186/silver-tungsten-electrodes-market

Significant Market Restraints Challenging Adoption

Despite their superior performance, several barriers can limit wider adoption of Silver Tungsten electrodes, especially in cost-sensitive markets and applications where alternative materials can provide acceptable performance.

-

Volatility in Raw Material Costs:

The Silver Tungsten Electrodes market is highly sensitive to price fluctuations in silver and tungsten. Both materials are globally traded commodities influenced by mining output, industrial demand, geopolitical tensions, energy costs, trade policies, and financial market activity.

Silver prices can be volatile due to demand from electronics, photovoltaics, investment markets, and industrial applications. Tungsten supply can also be affected by mining concentration, export policies, and regional production constraints. Price swings of 15-25% annually can create significant uncertainty for manufacturers and end-users.

Raw material volatility compresses manufacturer margins and complicates pricing strategies. For buyers, unpredictable electrode costs can affect procurement planning and operating budgets.

In cost-sensitive industries, this volatility may encourage users to explore alternative materials such as silver cadmium oxide, copper tungsten, or other contact materials. While these alternatives may not match Silver Tungsten’s performance in demanding applications, they can be attractive where cost pressure is high.

-

High Initial Investment and Manufacturing Complexity:

Producing high-quality Silver Tungsten electrodes requires sophisticated powder metallurgy processes. Manufacturers must carefully blend metal powders, control particle size, manage compaction, conduct high-temperature sintering, and ensure uniform microstructure throughout the final component.

These processes require controlled atmospheres, specialized sintering furnaces, advanced tooling, quality testing systems, and technical expertise. As a result, manufacturing costs can be 20-40% higher than for more conventional contact materials.

The capital intensity of production creates barriers for new entrants. Only specialized manufacturers with strong metallurgical knowledge and process control capabilities can produce consistent high-performance electrodes at scale.

This concentration of production among established players can limit supply chain flexibility and make customers dependent on a smaller supplier base. For end-users in electronics, automotive, aerospace, and industrial manufacturing, supplier reliability becomes a critical purchasing factor.

Critical Market Challenges Requiring Innovation

The journey from laboratory prototype to industrial-scale production presents several challenges that require continued innovation, quality control, and investment.

One of the most important technical challenges is achieving consistent material quality at high production volumes. Silver and tungsten have very different physical properties, making it difficult to achieve a perfectly homogeneous mixture and uniform sintered structure.

Batch-to-batch variation can affect conductivity, hardness, erosion resistance, porosity, and operating life. For high-precision applications such as EDM, semiconductor tooling, and electrical switching, even small variations can affect product performance.

Application-specific challenges also remain. In high-temperature DC applications, silver migration can reduce performance over time. In vacuum interrupters and high-voltage switching devices, porosity and contact structure must be carefully optimized to manage arc behavior and ensure reliability.

Leading manufacturers often spend 10-15% of revenue on research and development to address these technical issues. R&D focuses on improving powder blending, sintering control, microstructure uniformity, alloy design, and application-specific performance.

Supply chain complexity is another challenge. High-purity tungsten powder is essential because impurities can significantly reduce electrode performance and lifespan. The specialized nature of metal powders also creates logistics, storage, and handling requirements that add cost and operational complexity.

Vast Market Opportunities on the Horizon

-

Expansion of Renewable Energy Infrastructure:

The global expansion of renewable energy infrastructure presents a substantial opportunity for the Silver Tungsten Electrodes market. Solar farms, wind turbines, battery storage systems, power converters, and grid control systems all depend on reliable electrical switching and power management components.

Silver Tungsten electrodes are used in power electronics, contactors, switching devices, and control systems where reliability under variable loads is essential. Renewable energy systems often operate under fluctuating electrical conditions, making durable contact materials especially important.

Solar inverters and wind turbine control systems require components that can handle repeated switching, high current loads, and long operational lifetimes. Silver Tungsten’s arc erosion resistance and conductivity make it suitable for these demanding environments.

As global investments in solar and wind capacity continue reaching new records, demand for high-performance electrical contact and electrode materials is expected to increase. This creates long-term growth potential beyond traditional industrial manufacturing applications.

-

Development of Next-Generation Alloys:

The development of next-generation Silver Tungsten alloys represents another important opportunity. Research into nano-engineered alloys, improved powder metallurgy, and tertiary element additions is focused on improving electrical conductivity, mechanical strength, thermal stability, and arc erosion resistance.

The incorporation of elements such as carbon or nickel may help create composite materials with improved performance for specific applications. Nano-engineered structures could improve material uniformity and extend electrode service life.

These innovations may unlock new high-value uses in aerospace systems, military hardware, advanced medical devices, high-performance circuit protection, and next-generation industrial equipment.

As industries demand smaller, more reliable, and more power-dense components, advanced electrode materials with tailored properties will become increasingly valuable. Companies that successfully commercialize improved alloy systems may gain strong competitive advantages.

-

Strategic Partnerships and Vertical Integration:

Strategic partnerships between electrode manufacturers and end-user companies are becoming increasingly important. These collaborations help bridge the gap between material innovation and real-world industrial requirements.

By working directly with automotive OEMs, electronics manufacturers, semiconductor companies, and renewable energy equipment producers, electrode suppliers can develop application-specific solutions. This improves product fit, reduces qualification time, and supports long-term customer relationships.

For end-users, collaborative development ensures that electrodes meet exact requirements for conductivity, wear resistance, geometry, switching performance, and lifespan. For manufacturers, partnerships can secure long-term supply agreements and reduce market uncertainty.

Vertical integration is also becoming more relevant. Companies that control or closely coordinate raw material sourcing, powder processing, electrode production, and application support can better manage cost volatility and quality consistency.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented primarily by composition and performance properties, including:

● High Conductivity

● Low Conductivity

High Conductivity electrodes command the dominant market share because they offer an optimal balance of electrical performance, thermal resistance, and durability. These electrodes are widely used in precision applications such as EDM, fine welding, switching contacts, and micro-component manufacturing.

High Conductivity grades are especially important where stable arc behavior, minimal erosion, and reliable current transfer are required. Their ability to maintain performance under repeated thermal and electrical cycling makes them the preferred choice for demanding industrial applications.

Low Conductivity variants serve more specialized applications where controlled resistance is needed. These may include certain industrial processes, specialized switching systems, or applications where specific thermal and electrical behavior is required.

As end-use industries become more technically demanding, demand for customized Silver Tungsten compositions with tailored conductivity and erosion resistance is expected to grow.

By Application:

Key application segments include:

● Resistance Welding

● EDM (Electrical Discharge Machining)

● Electrical Contacts for Switching Devices

Resistance Welding remains a foundational application for Silver Tungsten electrodes. These electrodes are used where strong wear resistance, thermal stability, and conductivity are needed for repeated welding cycles. They are valuable in automotive components, electronics assembly, industrial fabrication, and precision joining applications.

EDM is demonstrating robust growth, driven by demand for complex precision tooling, molds, dies, and micro-machined components. The automotive, electronics, medical device, and semiconductor industries increasingly require intricate part geometries that can be produced accurately through electrical discharge machining.

Silver Tungsten electrodes are highly suitable for EDM because they offer dimensional stability, erosion resistance, and reliable performance during precision machining. As miniaturization and complex manufacturing increase, this segment is expected to remain a strong growth area.

Electrical Contacts for switching devices represent another important application. Silver Tungsten materials are used in circuit breakers, relays, contactors, vacuum interrupters, and high-voltage switches. Their arc erosion resistance and conductivity make them valuable in power distribution, industrial control, EV systems, and renewable energy infrastructure.

By End-User Industry:

The end-user landscape includes:

● Electronics & Semiconductor

● Automotive

● Aerospace

● Industrial Manufacturing

The Electronics & Semiconductor industry accounts for the largest share of demand. Silver Tungsten electrodes are used in micro-component welding, semiconductor tooling, EDM processes, electrical contacts, and precision manufacturing equipment. The growth of chips, sensors, displays, and consumer electronics supports continued demand.

The Automotive sector is rapidly emerging as a key growth engine. Electric vehicles, hybrid vehicles, battery systems, charging infrastructure, and advanced power electronics require durable contact materials for high-current switching and long-term reliability.

The Aerospace industry uses Silver Tungsten electrodes in high-reliability applications where material performance, durability, and resistance to extreme operating conditions are critical. Aerospace systems often require premium-grade components with strict quality standards.

Industrial Manufacturing continues to provide stable demand through resistance welding, EDM, circuit protection, machinery production, power systems, and precision tooling. As factories modernize and automation increases, demand for reliable electrode materials is expected to remain steady.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307186/silver-tungsten-electrodes-market

Frequently Asked Questions

What are Silver Tungsten electrodes used for?

Silver Tungsten electrodes are used in resistance welding, electrical discharge machining, circuit breakers, relays, contactors, high-voltage switching devices, semiconductor tooling, and precision manufacturing. They combine silver’s conductivity with tungsten’s hardness and arc erosion resistance, making them suitable for demanding electrical and thermal environments.

What is driving the Silver Tungsten Electrodes market?

The market is driven by rising demand from electronics manufacturing, semiconductor production, automotive electrification, EDM tooling, renewable energy infrastructure, and high-voltage switching systems. EV relays, battery management systems, solar inverters, and precision industrial manufacturing are creating new demand for durable electrode materials.

Which application is growing strongly in the Silver Tungsten Electrodes market?

EDM, or Electrical Discharge Machining, is showing strong growth due to rising demand for complex precision tooling, molds, dies, and micro-components. Automotive, electronics, semiconductor, and medical device manufacturers increasingly require accurate machining capabilities that benefit from Silver Tungsten electrode performance.

Why are Silver Tungsten electrodes preferred in high-performance applications?

Silver Tungsten electrodes are preferred because they offer high conductivity, strong thermal resistance, mechanical hardness, and excellent arc erosion resistance. This combination helps them maintain dimensional stability and reliability during repeated high-current, high-temperature, and high-precision operations.

Which region leads the Silver Tungsten Electrodes market?

Asia-Pacific leads the global Silver Tungsten Electrodes market, accounting for over 50% of consumption. The region’s dominance is supported by electronics manufacturing, semiconductor fabrication, automotive production, and strong industrial supply chains in China, Japan, South Korea, and other manufacturing hubs.

Competitive Landscape:

The global Silver Tungsten Electrodes market is semi-consolidated and marked by strong competition among specialized manufacturers. The market is dominated by companies with deep expertise in powder metallurgy, high-performance metals, precision manufacturing, and application-specific electrode design.

Leading players such as Metal Cutting Corporation and ChinaTungsten Online leverage advanced production capabilities, global distribution networks, technical know-how, and established customer relationships to maintain their market positions. Competition is primarily based on product quality, performance consistency, material purity, technical support, delivery reliability, and customization capability.

List of Key Silver Tungsten Electrodes Companies Profiled:

● Metal Cutting Corporation (U.S.)

● ChinaTungsten Online (Xiamen) (China)

● AEM Metal (U.S.)

● Holepop EDM (Japan)

● MWI, Inc. (U.S.)

● Mi-Tech Metals (U.S.)

● T&D Materials Manufacturing (U.S.)

● American Welding Products (U.S.)

● American Elements (U.S.)

● Luoyang Jiangchi Metal Material (China)

● Stanford Advanced Materials (U.S.)

The overarching competitive strategy revolves around heavy investment in research and development. Companies are focused on improving material performance, reducing manufacturing costs, extending electrode lifespan, and developing application-specific compositions.

Strategic partnerships with end-user companies are also becoming critical. By working with automotive OEMs, electronics manufacturers, semiconductor tooling companies, and renewable energy equipment suppliers, electrode manufacturers can validate new applications and secure long-term demand.

As industries require more reliable and customized electrode materials, companies with strong metallurgy expertise, advanced quality control, and flexible production capabilities are expected to strengthen their competitive positions.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific:

Asia-Pacific is the dominant force in the global Silver Tungsten Electrodes market, accounting for over 50% of global consumption. The region’s leadership is supported by its concentration of electronics manufacturing, semiconductor fabrication, automotive production, and industrial supply chains.

China plays a major role as both a producer and consumer. The country benefits from strong tungsten processing capacity, electronics manufacturing scale, and expanding industrial demand. Producers such as ChinaTungsten Online support the region’s supply base.

Japan and South Korea contribute strong demand through semiconductor manufacturing, precision electronics, automotive components, and advanced industrial applications. Their emphasis on quality and high-performance materials supports demand for premium Silver Tungsten electrodes.

The broader Asia-Pacific region also benefits from government support for advanced manufacturing, growing EV production, and increasing investment in semiconductor capacity. These factors are expected to keep the region at the center of global market demand.

● North America and Europe:

North America and Europe together represent a significant and technologically advanced secondary market bloc. Both regions have strong demand from aerospace, defense, automotive, electronics, industrial manufacturing, and precision engineering sectors.

North America’s demand is driven by high-tech aerospace, defense, EV power systems, semiconductor tooling, and advanced manufacturing applications. The region requires premium-grade Silver Tungsten electrodes for critical applications where reliability and performance are more important than lowest cost.

Europe’s market is characterized by demand from precision engineering, automotive manufacturing, industrial machinery, electrical systems, and advanced materials industries. Germany, France, Italy, and the UK contribute to regional consumption through high-quality manufacturing and engineering sectors.

Both regions emphasize strict quality standards, technical documentation, and application-specific solutions. Manufacturers serving these markets must demonstrate product consistency, traceability, and reliable technical support.

● South America, and Middle East & Africa:

South America, the Middle East, and Africa currently represent emerging markets for Silver Tungsten electrodes. Demand is primarily driven by industrialization, infrastructure development, power systems, mining, energy projects, and gradual expansion of local manufacturing capabilities.

South America shows potential through automotive production, mining equipment, industrial machinery, and power infrastructure development. Brazil is one of the more important regional markets due to its industrial base.

The Middle East is investing in energy infrastructure, industrial diversification, and manufacturing capacity. These developments may gradually create demand for high-performance electrical contacts and electrode materials.

Africa remains smaller in scale but may present future opportunities as industrial manufacturing, power distribution, mining, and infrastructure sectors develop. Over time, increasing modernization of electrical and industrial systems could support market growth.

Get Full Report Here:

https://www.24chemicalresearch.com/reports/307186/silver-tungsten-electrodes-market

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307186/silver-tungsten-electrodes-market

Need More In-Depth Market Intelligence?

The complete report provides detailed insights into:

✔ Regional demand forecasts

✔ Production capacity analysis

✔ Pricing trends

✔ Competitive landscape

✔ Supply chain developments

✔ Emerging opportunities

✔ Product type analysis

✔ Application-wise growth outlook

✔ Raw material cost and supply trends

Access the Full Report:

https://www.24chemicalresearch.com/reports/307186/silver-tungsten-electrodes-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a trusted provider of chemical market intelligence, serving clients including over 30 Fortune 500 companies. The company provides data-driven insights through rigorous research methodologies, helping businesses understand government policy, emerging technologies, competitive landscapes, production capacity, pricing movements, and supply chain developments.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030