High Purity Antimony Metal Market to Reach USD 2.75 Billion by 2034 as Electronics and Battery Applications Expand

High purity antimony metal, typically defined as antimony with purity levels of 99.5% (2N5) or higher, has become an increasingly important material for industries that require precise chemical composition, stable performance, and controlled impurity levels. Although antimony has long been used in traditional industrial applications, high purity grades are now gaining stronger relevance in advanced electronics, semiconductor manufacturing, flame retardant systems, energy storage, and specialized metal alloys.

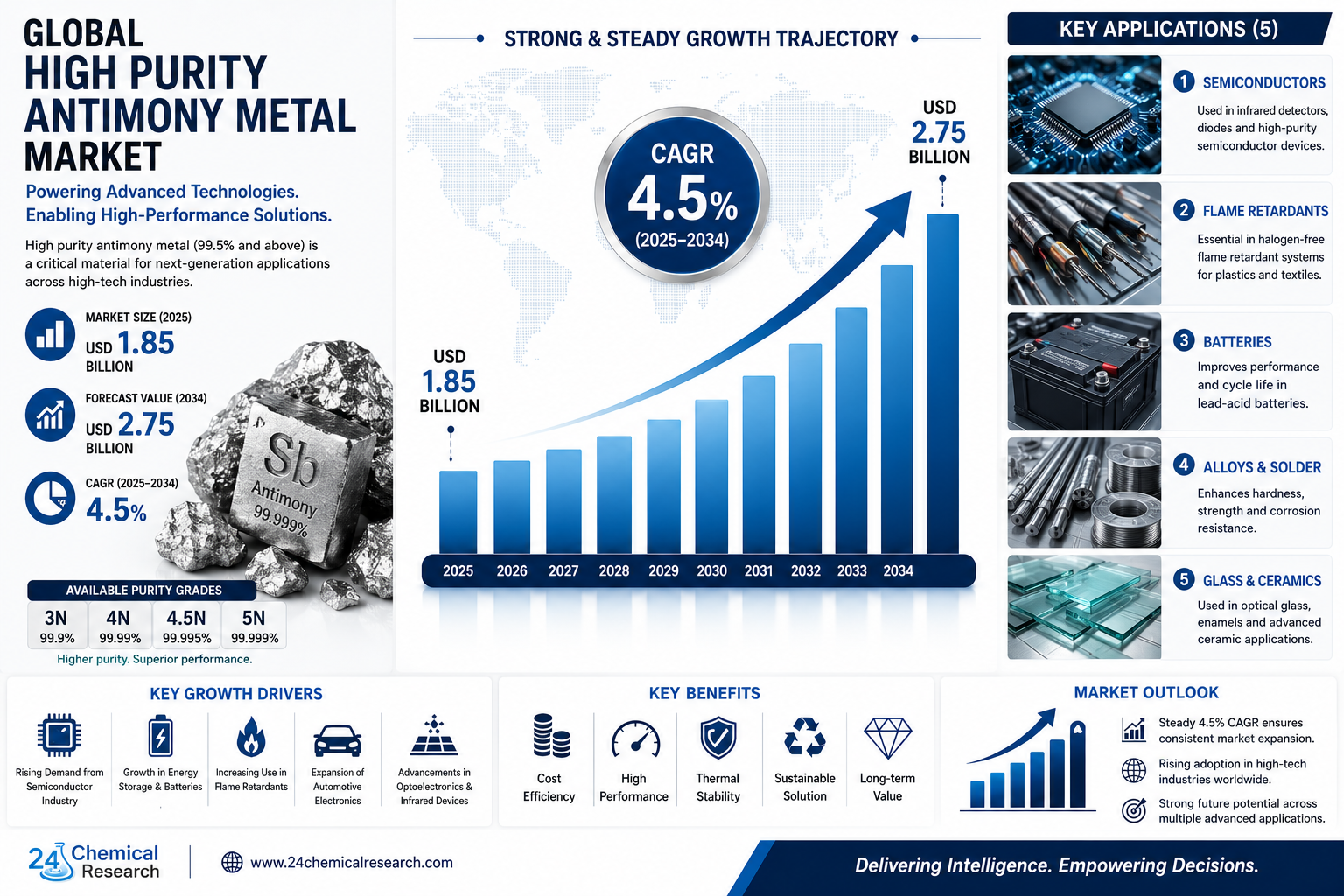

What makes high purity antimony metal valuable is its unique combination of hardening ability, semiconductor behavior, thermal stability, and compatibility with specialized chemical and metallurgical processes. Commercial grades include 3N (99.9%), 4N (99.99%), 4.5N (99.995%), 5N (99.999%), and other customized purity levels. Higher purity grades command significant price premiums because they require advanced refining technologies, stricter quality control, and more precise impurity management.

Global High Purity Antimony Metal Market was valued at USD 1.85 billion in 2025 and is projected to reach USD 2.75 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 4.5% during the forecast period. The market’s expansion is closely linked to rising demand from semiconductor devices, flame retardant formulations, automotive batteries, energy storage systems, and advanced manufacturing sectors where material purity directly affects performance and reliability.

Get Full Report Here:

https://www.24chemicalresearch.com/reports/307148/high-purity-antimony-metal-market

Market Dynamics:

The High Purity Antimony Metal market is shaped by a complex mix of semiconductor demand, fire safety regulations, battery technology requirements, supply chain concentration, environmental compliance, and emerging opportunities in recycling and advanced materials. As industries move toward higher-performance materials and more secure supply chains, high purity antimony is becoming strategically important for both traditional and next-generation applications.

Key Market Highlights

● Global High Purity Antimony Metal Market was valued at USD 1.85 billion in 2025 and is projected to reach USD 2.75 billion by 2034.

● The market is expected to grow at a CAGR of 4.5% during the forecast period.

● Electronics and semiconductors represent one of the strongest growth areas due to antimony’s role in doping, infrared detectors, and high-performance electronic components.

● Flame retardants remain a major volume-driven application, supported by global fire safety regulations across construction, transportation, and electronics sectors.

● 4.5N purity antimony is emerging as a highly dynamic segment because it offers a strong balance between performance and production economics.

● Asia-Pacific dominates both production and consumption, supported by China’s antimony reserves, refining capacity, and electronics manufacturing base.

● Recycling, geographic supply diversification, and advanced semiconductor applications represent important long-term opportunities.

Powerful Market Drivers Propelling Expansion

-

Electronics and Semiconductor Industry Demand:

The electronics and semiconductor industry is one of the most important demand drivers for the High Purity Antimony Metal market. In semiconductor manufacturing, high purity antimony is used in doping applications, silicon wafer processing, infrared detectors, and specialized electronic materials where impurity control is critical.

The global semiconductor industry, valued at approximately $600 billion, continues to require materials that support device miniaturization, improved conductivity, thermal stability, and high-frequency performance. Antimony plays an important role in improving electron mobility and enhancing the performance of selected semiconductor devices.

As 5G infrastructure, Internet of Things devices, sensors, communication equipment, and high-frequency electronic systems continue to expand, demand for antimony-based components is expected to strengthen. In these applications, material purity directly affects device efficiency, performance consistency, and reliability. This makes high purity antimony metal especially important for advanced electronics manufacturers that require stable and precisely engineered materials.

The growth of artificial intelligence hardware, automotive electronics, industrial automation, and smart devices is also increasing semiconductor content across end-use industries. As electronic systems become more complex and performance-sensitive, demand for higher-purity specialty materials such as 4N, 4.5N, and 5N antimony is expected to rise.

-

Flame Retardant Applications:

Flame retardant applications continue to provide a stable demand base for high purity antimony metal. Antimony trioxide, which is derived from antimony metal, is widely used as a synergist in halogenated flame retardant systems. It helps improve flame suppression performance in plastics, textiles, coatings, rubber, electronics, building materials, and transportation components.

Fire safety regulations are becoming more stringent across construction, automotive, electronics, electrical equipment, and consumer goods sectors. These regulations increase the need for effective flame retardant materials that can reduce ignition risk, slow flame spread, and improve product safety.

The global flame retardants market is projected to exceed $12 billion by 2030, and antimony-based formulations remain important because they can demonstrate 20-30% greater efficacy compared to several alternative solutions. This performance advantage supports continued use in applications where fire safety, cost efficiency, and material compatibility are essential.

Although environmental concerns around halogenated flame retardants are encouraging development of alternative systems, antimony-based flame retardants remain widely used in regulated applications where performance requirements are strict. This keeps the segment relevant and provides consistent volume demand for the High Purity Antimony Metal market.

-

Energy Storage Innovations:

Energy storage applications represent another important growth area for high purity antimony metal. While lithium-ion batteries dominate portable electronics and electric vehicles, lead-acid batteries remain essential in automotive starting systems, backup power, industrial energy storage, telecom infrastructure, and uninterruptible power supply systems.

Antimony is used to harden lead grids in lead-acid batteries, improving mechanical strength, deep-cycle performance, durability, and operational reliability. Antimony-enhanced batteries are particularly valuable in applications requiring dependable power delivery under demanding conditions.

Recent advancements in battery technology show that antimony additives can improve cycle life by 15-25% in industrial applications. This helps maintain the relevance of antimony-based batteries, especially in markets where cost-effectiveness, recyclability, reliability, and established infrastructure are important.

In addition to traditional lead-acid systems, antimony is being studied for advanced energy storage technologies and specialized battery chemistries. As grid storage, renewable energy integration, and industrial backup power demand continue to increase, antimony’s role in durable battery materials may create additional opportunities.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307148/high-purity-antimony-metal-market

Significant Market Restraints Challenging Adoption

Despite its critical applications, the High Purity Antimony Metal market faces substantial hurdles that limit growth potential and create operational challenges for producers, refiners, and end-users.

-

Supply Chain Concentration Risks:

One of the most serious restraints in the High Purity Antimony Metal market is supply chain concentration. China controls approximately 70% of global antimony production and refining capacity, making the market highly exposed to geographic, geopolitical, and policy-related risks.

This concentration creates vulnerability for downstream industries that depend on consistent antimony supply. Electronics manufacturers, flame retardant producers, battery companies, and advanced materials suppliers may face disruptions caused by export restrictions, trade disputes, environmental inspections, logistics challenges, or policy changes.

Recent trade policy fluctuations have shown how quickly supply disruptions can affect pricing. During periods of export constraint, antimony price volatility can reach 25-40%, creating uncertainty for buyers and discouraging long-term investment in antimony-dependent technologies.

For Western manufacturers, this supply concentration has become a strategic concern. Many companies are now evaluating alternative sources, recycling options, and supply agreements to reduce exposure to single-region dependency. However, developing new antimony production and refining capacity outside China requires time, capital, technical expertise, and regulatory approval.

-

Environmental and Regulatory Pressures:

Antimony mining and processing face increasing environmental scrutiny due to concerns related to mining byproducts, waste streams, water contamination, emissions, and toxicity risks. As environmental regulations become stricter, producers must invest in cleaner processing systems, waste management, water treatment, and monitoring technologies.

Compliance costs have risen 15-20% annually in major producing regions as regulators impose tighter environmental requirements. These rising costs can affect profitability, delay projects, and increase final product pricing.

In the European Union and North America, antimony’s classification as a substance of concern under regulatory frameworks such as REACH creates additional compliance burdens. Producers and downstream users must provide documentation, safety data, exposure assessments, and environmental impact information to meet regulatory requirements.

New mining and refining projects face long approval timelines. Environmental impact assessments for new antimony operations can require 24-36 months, significantly delaying capacity expansion. These delays make it difficult for the market to respond quickly to rising demand from semiconductors, energy storage, and flame retardant applications.

Critical Market Challenges Requiring Innovation

The transition from traditional antimony applications to high-tech uses presents unique challenges that require process innovation, investment in refining technology, and stronger quality control.

Production of ultra-high purity antimony, especially 4N, 4.5N, and 5N grades, requires sophisticated refining techniques. These processes are energy-intensive, technically complex, and highly sensitive to contamination. Even small impurity levels can affect semiconductor performance, optical properties, electronic behavior, or alloy stability.

Maintaining consistent quality at commercial scale remains difficult. Even advanced refining facilities may experience batch-to-batch variations that can affect up to 15% of production output. For semiconductor and electronics customers, this level of variation can create qualification challenges, yield issues, and additional testing requirements.

The capital expenditure required for precision refining equipment is another major barrier. New high-purity antimony refining facilities may require investments of $50-100 million to operate at economically viable scale. This limits the number of new entrants and reinforces the position of established producers with technical expertise and existing infrastructure.

The market also faces substitution threats across multiple applications. In flame retardants, non-halogenated alternatives are gaining attention due to environmental and regulatory concerns. Although some alternatives have performance limitations, they are increasingly used in applications where sustainability requirements or regulatory pressure are strong.

In batteries, lithium-ion technology continues to replace lead-acid batteries in many mobility and energy storage applications. While antimony-enhanced lead-acid batteries remain important for specific use cases, especially where durability and cost matter, producers must continue proving their value against competing battery chemistries.

These challenges require antimony producers to focus on performance differentiation, purity improvement, recycling, supply reliability, and application-specific material development.

Vast Market Opportunities on the Horizon

-

Advanced Semiconductor Applications:

Advanced semiconductor applications represent one of the most attractive opportunities for the High Purity Antimony Metal market. As semiconductor devices continue to shrink and operate at higher performance levels, demand for ultra-high purity materials is increasing.

Antimony-based materials are being explored for next-generation doping applications, compound semiconductors, infrared detectors, thin films, and specialized electronic components. Research indicates that antimony-based materials could support next-generation transistors with improved electron mobility and better thermal characteristics.

Antimony-based thin films also show potential in photovoltaic applications. Emerging photovoltaic technologies are seeking materials that can improve efficiency, stability, and manufacturability compared to traditional silicon-based systems. High purity antimony may play a role in selected thin-film and compound semiconductor technologies.

As 5G, AI hardware, advanced sensors, aerospace electronics, and high-frequency devices expand, demand for high-purity antimony grades may increase. This creates opportunities for suppliers that can consistently produce 4N, 4.5N, and 5N antimony with tight impurity control.

-

Geographic Supply Diversification:

The current concentration of antimony supply creates strong opportunities for developing production capacity outside China. Countries with known antimony resources, including Australia, Canada, Bolivia, and selected other regions, are attracting attention from investors and end-users seeking more secure supply chains.

Geographic diversification can reduce geopolitical risk, improve procurement stability, and support customers that want regional or non-China sources of critical materials. This is especially important for industries such as semiconductors, defense, energy storage, and advanced manufacturing, where supply continuity is strategically important.

New projects outside China also offer an opportunity to implement more sustainable production methods from the beginning. Facilities that use advanced water recycling, waste management, cleaner refining technologies, and lower-emission processes may appeal to environmentally conscious customers.

Producers that can combine reliable supply, high purity levels, and strong environmental standards may be able to command premium pricing. This is particularly relevant as customers increasingly evaluate suppliers based on sustainability, traceability, and supply chain security.

-

Recycling and Circular Economy Initiatives:

Recycling represents a major long-term opportunity for the High Purity Antimony Metal market. As sustainability becomes more important, manufacturers are increasingly looking for ways to recover critical materials from electronic waste, flame-retardant-containing plastics, spent batteries, industrial residues, and metallurgical byproducts.

Advanced recycling technologies can recover high purity antimony from end-of-life products with recovery rates exceeding 90%. This creates a secondary supply stream that can reduce dependence on primary mining and improve supply chain resilience.

Closed-loop recycling systems are especially attractive for electronics, battery, and flame retardant manufacturers seeking to improve sustainability credentials. Recovered antimony can help reduce waste, lower environmental impact, and support circular economy goals.

As regulations around electronic waste and critical material recovery become stricter, recycling could become an increasingly important source of high purity antimony supply. Companies that develop scalable and cost-effective recycling processes may gain a strong competitive advantage.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into:

● 3N Purity

● 4N Purity

● 4.5N Purity

● 5N Purity

● Others

4.5N Purity currently represents one of the most dynamic segments in the High Purity Antimony Metal market. This grade offers an optimal balance between performance and production economics, making it suitable for semiconductor applications, advanced electronic components, and specialized industrial uses.

4.5N antimony provides sufficient purity for many high-performance electronic applications while remaining more economically viable than ultra-premium 5N grades. This makes it attractive for manufacturers that require strong material performance but must also manage production costs.

The 5N Purity segment, while smaller in volume, commands significant price premiums. It is used in highly specialized applications where even minimal impurity levels can affect performance. These may include advanced semiconductor materials, infrared detectors, thin films, and research-grade applications.

3N and 4N purity grades continue to serve important industrial and electronic applications where extremely high purity is not always required. These grades provide a practical balance of cost, availability, and performance for flame retardant precursors, selected alloys, battery applications, and industrial processing.

By Application:

Application segments include:

● Electronics and Semiconductors

● Flame Retardants

● Lead-Acid Batteries

● Others

The Electronics and Semiconductors segment demonstrates the strongest growth momentum. Demand is driven by semiconductor fabrication, infrared detectors, 5G devices, IoT equipment, advanced sensors, and high-frequency electronic systems. In these applications, purity directly affects performance, making high-purity antimony grades essential.

Flame Retardants remain the largest application by volume. Antimony trioxide derived from antimony metal is widely used as a synergist in halogenated flame retardant systems. Construction materials, electronics, transportation components, cables, plastics, and textiles continue to require effective flame suppression materials to meet safety standards.

Lead-Acid Batteries represent a stable application segment. Antimony-hardened grids improve durability and deep-cycle performance, making them relevant for automotive starting batteries, industrial backup power, telecom power systems, and selected energy storage applications.

Other applications include specialty alloys, catalysts, glass manufacturing, pigments, military applications, and advanced materials research. These applications may represent smaller volumes but can offer attractive margins when high purity or specialized performance is required.

By End-User Industry:

The end-user landscape includes:

● Electronics Manufacturing

● Automotive

● Construction

● Energy Storage

Electronics Manufacturing accounts for the most significant share of high purity demand. Semiconductor companies, component manufacturers, sensor producers, and electronics material suppliers use high purity antimony in applications where consistent composition and controlled impurities are critical.

The Automotive sector remains important due to both battery applications and flame retardant use in vehicle interiors, wiring, plastics, and electronic systems. As vehicles become more electrified and electronically complex, demand for high-performance materials is expected to remain steady.

The Construction industry uses antimony-based flame retardant systems in building materials, insulation, coatings, wiring, and polymer products. Stricter fire safety regulations support ongoing demand in this segment.

Energy Storage shows promising growth potential as demand for backup power, industrial batteries, renewable energy integration, and grid storage increases. While lithium-ion batteries dominate many emerging applications, antimony-enhanced lead-acid batteries remain relevant where durability, recyclability, and cost-effectiveness are important.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307148/high-purity-antimony-metal-market

Frequently Asked Questions

What is High Purity Antimony Metal used for?

High purity antimony metal is used in semiconductors, flame retardants, lead-acid batteries, specialty alloys, infrared detectors, electronic components, and advanced materials. Its properties, including hardening ability, semiconductor behavior, and thermal stability, make it valuable in applications where controlled purity and consistent performance are important.

What is driving the High Purity Antimony Metal market?

The High Purity Antimony Metal market is driven by rising demand from electronics, semiconductor manufacturing, flame retardants, lead-acid batteries, energy storage, and advanced materials. Growth in 5G infrastructure, IoT devices, automotive electronics, and stricter fire safety regulations is increasing demand for high-purity antimony grades.

Which purity grade is growing fastest in the market?

4.5N purity antimony is one of the most dynamic segments because it offers a strong balance between high performance and production economics. It is suitable for many semiconductor and advanced electronics applications while remaining more cost-effective than ultra-high purity 5N grades.

Which region dominates the High Purity Antimony Metal market?

Asia-Pacific dominates the High Purity Antimony Metal market, accounting for more than 70% of production and consumption. China leads due to its antimony reserves, refining capacity, and strong electronics manufacturing base, while Japan and South Korea contribute significant demand for high-purity semiconductor grades.

What challenges affect the High Purity Antimony Metal industry?

Key challenges include supply chain concentration, environmental regulations, high refining costs, quality consistency issues, and substitution risks in flame retardants and batteries. The production of ultra-high purity antimony requires advanced technology, significant capital investment, and strict impurity control.

Competitive Landscape:

The global High Purity Antimony Metal market is moderately consolidated, with strong competition between established producers and emerging players. The market is influenced by production capacity, access to antimony resources, refining technology, purity control, customer relationships, and geographic supply reliability.

The top three companies—Hunan Gold Group (China), Hsikwang Shan Twinking Star (China), and Mandalay Resources (Canada)—collectively command approximately 45% of the market share as of 2025. Their dominance is supported by vertical integration, extensive technical expertise, resource access, and long-term customer relationships across electronics, flame retardants, batteries, and specialty materials.

List of Key High Purity Antimony Metal Companies Profiled:

● Hunan Gold Group (China)

● Hsikwang Shan Twinking Star (China)

● Mandalay Resources (Canada)

● Dongfeng (China)

● Hechi Nanfang Non-ferrous Metals Group (China)

● GeoProMining (Russia)

● China-Tin Group (China)

● Anhua Huayu Antimony Industry (China)

● Huachang Group (China)

● Yongcheng Antimony Industry (China)

● Geodex Minerals (Canada)

● United States Antimony (USA)

Competitive strategy focuses heavily on technological innovation, purity improvement, production efficiency, and supply chain security. Established producers are investing in research and development to improve refining yields, reduce impurities, lower production costs, and meet the increasing purity requirements of semiconductor and electronics customers.

Strategic partnerships with end-users are also becoming more important. Semiconductor manufacturers, battery companies, flame retardant producers, and advanced materials firms often require customized specifications and consistent supply. Producers that can offer technical support, quality documentation, and application-specific material grades are better positioned to secure long-term contracts.

Newer entrants are focusing on niche applications, geographic diversification, recycling, and markets that are underserved by larger producers. As buyers seek alternatives to China-dominated supply, companies with resources in Canada, Australia, Bolivia, and other regions may benefit from growing interest in supply chain resilience.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific:

Asia-Pacific dominates the global High Purity Antimony Metal market, holding more than 70% of both production and consumption. China’s position as the leading production hub is supported by extensive antimony reserves, established mining and refining infrastructure, and strong domestic demand from electronics, flame retardants, batteries, and chemical manufacturing.

China’s dominance gives the region a major cost and capacity advantage, but it also creates global supply concentration concerns. Many downstream industries depend heavily on Chinese antimony supply, making Asia-Pacific central to both market growth and supply chain risk.

Japan and South Korea contribute significant demand for high purity antimony grades, especially in semiconductor and electronics applications. These countries have advanced electronics, semiconductor, battery, and specialty materials industries that require consistent, high-quality antimony supply.

Southeast Asia is emerging as an important consumption center as electronics manufacturing expands across countries such as Vietnam, Malaysia, Thailand, and Indonesia. As global companies diversify production networks, regional demand for high purity antimony materials may continue to increase.

● North America:

North America represents the second-largest market for High Purity Antimony Metal, driven by demand from semiconductors, aerospace, defense, energy storage, flame retardants, and advanced materials. The United States recognizes antimony as an important material for defense, critical infrastructure, and industrial security.

Although domestic antimony production is limited, North America has strong technical capabilities in purification, processing, materials engineering, and high-value applications. This supports regional demand for higher-purity grades used in semiconductors, defense electronics, specialty alloys, and advanced manufacturing.

The United States maintains strategic stockpiles of antimony because of its importance in defense and critical applications. Recent initiatives to develop domestic and regional sources reflect growing concern about supply chain security and dependence on imported materials.

Canada also plays an important role through companies such as Mandalay Resources and emerging mineral development projects. As supply diversification becomes more important, North American projects may attract greater investment.

● Europe:

Europe shows steady demand for High Purity Antimony Metal, primarily from automotive, construction, electronics, flame retardants, and specialty chemical applications. Germany and France lead regional consumption because of their strong automotive, chemical, industrial, and electronics sectors.

The region’s strict environmental regulations influence both demand and sourcing decisions. European buyers often require high-purity materials that meet performance standards while complying with safety, environmental, and chemical regulations.

Antimony-based flame retardants remain important in construction materials, automotive components, electrical equipment, cables, and polymer applications. However, environmental pressure is encouraging greater interest in safer formulations, recycling, and responsible sourcing.

Europe has limited primary antimony production capacity, making the region heavily dependent on imports, particularly from China. This dependence has increased interest in recycling, secondary recovery, and alternative supply sources to improve long-term material security.

Get Full Report Here:

https://www.24chemicalresearch.com/reports/307148/high-purity-antimony-metal-market

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307148/high-purity-antimony-metal-market

Need More In-Depth Market Intelligence?

The complete report provides detailed insights into:

✔ Regional demand forecasts

✔ Production capacity analysis

✔ Pricing trends

✔ Competitive landscape

✔ Supply chain developments

✔ Emerging opportunities

✔ Segment-wise growth outlook

✔ Purity-grade demand analysis

✔ Technology and application trends

Access the Full Report:

https://www.24chemicalresearch.com/reports/307148/high-purity-antimony-metal-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a trusted provider of chemical market intelligence, serving clients including over 30 Fortune 500 companies. The company provides data-driven insights through rigorous research methodologies, helping businesses understand government policy, emerging technologies, competitive landscapes, production capacity, pricing movements, and supply chain developments.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030