Automotive Control Arm Market Outlook and Size Analysis Reaching 39.13 Billion USD by 2034

The automotive component manufacturing industry serves as the backbone of global vehicle production, ensuring that ride comfort, directional stability, and passenger safety meet modern regulatory standards. Within a vehicle's suspension assembly, the control arm plays an indispensable role. It acts as the primary mechanical hinge connecting the wheel hub and steering knuckles to the vehicle’s chassis or frame. By regulating wheel synchronization and dampening structural vibration, the control arm directly governs handling precision and tread wear. Driven by persistent shifts in global automotive demand, structural vehicle redesigns, and expanding replacement cycles, the global market for automotive control arms is preparing for a decade of steady growth.

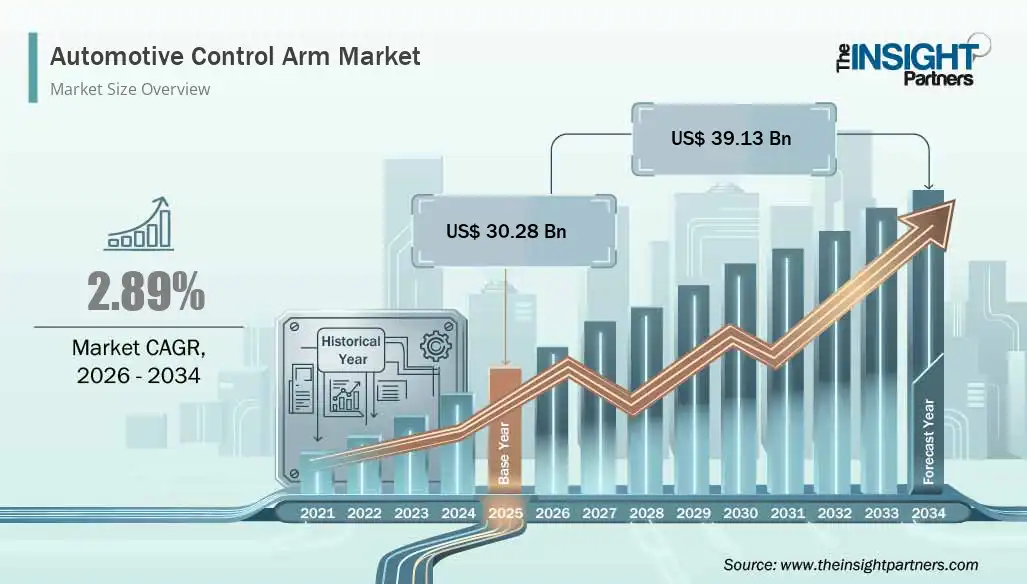

Market Valuation and Growth Trajectory

According to a comprehensive industry study by The Insight Partners, the automotive control arm market is positioned for significant economic expansion over the next decade. The Automotive Control Arm Market size is expected to reach US$ 39.13 Billion by 2034 from US$ 30.28 Billion in 2025. This steady long-term appreciation translates into a steady upward trajectory, with the market anticipated to register a CAGR of 2.89% during the forecast period 2026–2034.

This growth is fueled by a dual-demand mechanism: the rising production volumes of passenger and commercial vehicles in developing industrial clusters, alongside a robust aftermarket driven by routine component wear. Control arms, being subject to constant mechanical stress, road debris, and structural fatigue, require ongoing maintenance and replacement. This dynamic ensures a reliable, predictable demand lifecycle that protects component suppliers even during fluctuations in new car sales.

Key Market Drivers and Technological Influences

Several structural factors are reshaping the production and material selection parameters for automotive control arms worldwide:

-

Vehicle Lightweighting Initiatives: To comply with increasingly stringent corporate average fuel economy (CAFE) policies and greenhouse gas emission limits, original equipment manufacturers (OEMs) are actively shedding vehicle curb weight. Consequently, heavy cast iron or stamped steel control arms are rapidly being replaced by advanced aluminum alloys, forged aluminum, and lightweight high-strength composite materials.

-

The Rise of Electric Vehicles (EVs): The global automotive shift toward battery electric vehicle architectures introduces distinct structural challenges. EVs carry heavy lithium-ion battery packs, requiring suspension systems that can handle increased weight and localized torque loads. Manufacturers are adapting by designing heavy-duty control arm configurations that balance durability with the lightweight profiles required to optimize battery range.

-

Expansion of Global Infrastructure: The rising volume of commercial logistics, long-haul freight operations, and public transport infrastructure across emerging economies is increasing the wear-and-tear rate of chassis parts. This expansion drives substantial aftermarket sales for heavy-duty suspension linkages and control arm kits designed for commercial applications.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00017711

Prominent Industry Key Players

The competitive landscape of the automotive control arm market features an integrated mix of multinational tier-1 suspension suppliers and specialized aftermarket manufacturers. These entities maintain market share by focusing on structural rigidity, precision casting, and expanded distribution networks.

Key players operating in the global market include:

-

A ONE Parts Co., Ltd.

-

Alltech Automotive

-

CCYS

-

Lemdor Control Arm Co., Ltd.

-

Magneti Marelli

-

MZW Motor

-

Nalbro Auto Parts Pvt. Ltd.

-

RTS S.A.

-

TRW Automotive Holdings Corp

-

ZF Friedrichshafen AG

Future Outlook

Looking forward, the automotive control arm market is set to undergo an extensive technical transition. Component designs will move beyond traditional mechanical shapes to adopt geometric optimizations developed through computer-aided engineering and generative design algorithms. This evolution will focus heavily on reducing unsprung mass without sacrificing structural integrity or crashworthiness.

Furthermore, as autonomous fleets and ride-sharing operations gain ground globally, individual vehicle utilization rates will rise dramatically. This shift will compress part replacement cycles and place a premium on high-durability, premium-grade control arms. Over the 2026–2034 forecast period, the market will increasingly reward manufacturers who successfully blend lightweight material processing with intelligent, automated supply chain management to serve both high-volume OEM assembly lines and highly fragmented global aftermarket channels.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876