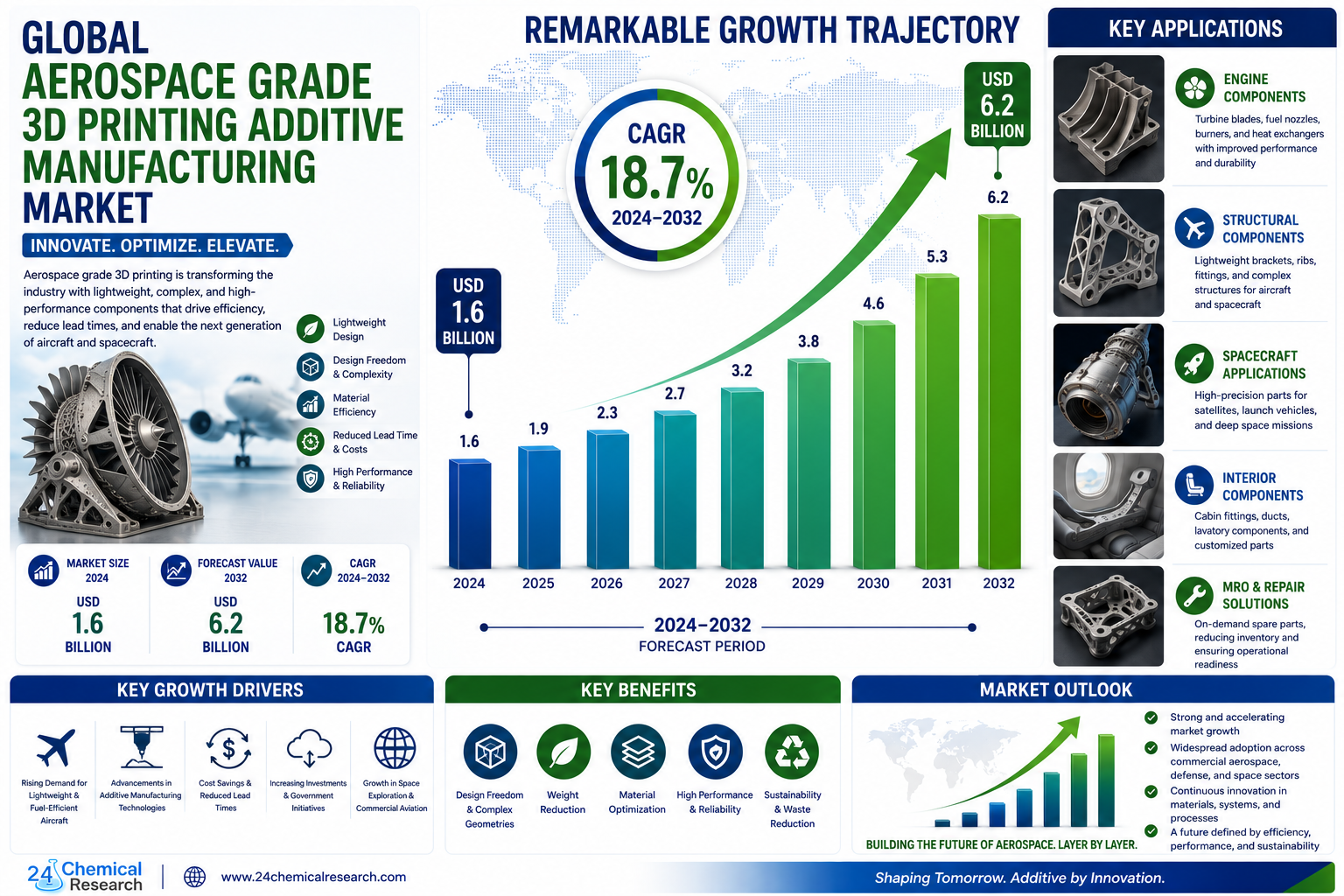

Global Aerospace Grade 3D Printing Additive Manufacturing market was valued at USD 1.6 billion in 2024 and is projected to reach USD 6.2 billion by 2032, exhibiting a remarkable CAGR of 18.7% during the forecast period.

Aerospace Grade 3D Printing Additive Manufacturing has evolved from an innovative prototyping technology into a fundamental pillar of modern aerospace production. The technology enables manufacturers to create lightweight, highly complex, and structurally optimized components that are impossible to produce using conventional manufacturing methods. By utilizing advanced metal alloys, high-performance polymers, and certified additive manufacturing processes, aerospace companies are achieving substantial reductions in weight, production lead times, and supply chain complexity.

The increasing adoption of additive manufacturing across commercial aviation, defense programs, and the rapidly expanding space industry is positioning the technology as one of the most transformative developments in advanced manufacturing.

Get Full Report Here: https://www.24chemicalresearch.com/reports/268669/global-aerospace-grade-d-printing-additive-forecast-market-2024-2030-729

Key Takeaways

● Commercial aviation remains the largest end-user segment.

● Engine components account for the leading application category.

● Metal materials dominate due to their strength and thermal performance.

● North America leads the global market with strong aerospace manufacturing capabilities.

● Space exploration and MRO services present major future growth opportunities.

● Strategic collaborations between OEMs and technology providers continue to accelerate adoption.

Market Overview & Regional Analysis

North America currently dominates the Aerospace Grade 3D Printing Additive Manufacturing market, accounting for approximately 52% of global activity. The region benefits from a highly developed aerospace ecosystem, significant research and development investments, and the presence of leading aircraft manufacturers, defense contractors, and space technology companies. The United States remains at the forefront of additive manufacturing innovation, with extensive deployment across commercial, military, and space applications.

Europe represents the second-largest regional market, supported by flagship aerospace programs and advanced materials science expertise. Germany, the United Kingdom, and France continue to invest heavily in additive manufacturing technologies as aerospace companies seek greater production efficiency and sustainability.

Asia-Pacific is rapidly emerging as a strategic growth market. China, Japan, Singapore, and South Korea are strengthening domestic aerospace manufacturing capabilities through government-backed initiatives and investments in advanced manufacturing infrastructure. Growing defense expenditures and expanding commercial aviation industries further contribute to regional demand.

Key Market Drivers and Opportunities

1. Transformation of Aerospace Component Manufacturing

The aerospace industry continues to embrace additive manufacturing for production-grade components due to its ability to significantly reduce weight while maintaining exceptional structural performance. Complex components such as turbine blades, fuel nozzles, heat exchangers, and structural brackets can now be manufactured with optimized geometries that traditional manufacturing methods cannot achieve.

Aircraft manufacturers increasingly incorporate thousands of additive-manufactured components into modern aircraft platforms, helping reduce fuel consumption, lower emissions, and shorten production cycles.

2. Advancements in Materials Science and Certification

Continuous innovation in aerospace-grade materials is expanding the capabilities of additive manufacturing. Advanced titanium alloys, nickel-based superalloys, aluminum alloys, and high-performance polymers are being specifically engineered for additive processes.

Recent certifications by aviation authorities have enabled broader use of additive-manufactured components in flight-critical applications. Enhanced fatigue resistance, improved thermal performance, and superior material consistency are driving greater acceptance throughout the aerospace industry.

3. Supply Chain Optimization and Digital Manufacturing

Digital inventory and distributed manufacturing models are transforming aerospace logistics. Additive manufacturing enables companies to produce components on demand, reducing inventory costs and minimizing supply chain disruptions.

This capability is particularly valuable for low-volume replacement parts and aging aircraft fleets, where maintaining traditional tooling and inventory becomes economically inefficient. Digital warehousing strategies also improve operational resilience by reducing dependency on complex global supply chains.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/268669/global-aerospace-grade-d-printing-additive-forecast-market-2024-2030-729

Challenges & Restraints

High Equipment and Material Costs

Industrial aerospace-grade additive manufacturing systems require substantial capital investments, with advanced metal printing platforms often costing several million dollars. Specialized metal powders and post-processing operations such as heat treatment, machining, and quality inspection further increase overall production costs.

These economic barriers continue to limit widespread adoption for certain component categories.

Regulatory and Certification Complexity

The aerospace industry maintains some of the world's strictest certification standards. Qualifying new additive manufacturing materials and processes requires extensive testing, validation, and documentation, often extending development timelines significantly.

The absence of universally standardized certification frameworks across multiple jurisdictions adds further complexity for global aerospace manufacturers.

Production Scale and Workforce Limitations

Maintaining consistent quality across multiple production systems remains a technical challenge. Additionally, the limited availability of skilled engineers and technicians with expertise in both additive manufacturing and aerospace engineering continues to create workforce shortages that may slow industry expansion.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Material Type:

The market is segmented into:

● Plastics Material

● Ceramics Material

● Metals Material

● Others

Metals Material currently dominates the market due to its critical role in manufacturing high-strength engine components and structural aerospace parts. Titanium and nickel-based alloys remain among the most widely adopted materials for additive manufacturing.

By Application:

Application segments include:

● Engine Components

● Structural Components

● Interior Components

● Others

Engine Components currently represent the largest application segment, benefiting from additive manufacturing's ability to create highly complex internal cooling channels and optimized lightweight structures. Structural Components are expected to witness the highest growth over the coming years.

By End-User Industry:

The end-user landscape includes:

● Commercial Aviation

● Defense Aviation

● Space

● Others

Commercial Aviation accounts for the largest market share, while the Space sector is emerging as one of the fastest-growing end-user categories due to increasing investments in commercial space exploration and satellite manufacturing.

Competitive Landscape

The global Aerospace Grade 3D Printing Additive Manufacturing market remains highly competitive and innovation-driven. Leading companies continue to focus on expanding material portfolios, improving production reliability, and forming strategic partnerships with aerospace OEMs to accelerate certification and commercialization.

Research and development investments remain a central competitive strategy as manufacturers work to enhance process consistency, reduce production costs, and expand application possibilities.

Key Companies Profiled

● Stratasys (U.S.)

● 3D Systems (U.S.)

● GE Additive (U.S.)

● Arcam Group (Sweden)

● Renishaw (U.K.)

● ExOne (U.S.)

● Optomec (U.S.)

● SLM Solutions (Germany)

● EnvisionTEC (Germany)

● VoxelJet AG (Germany)

● Sciaky Inc (U.S.)

● EOS GmbH (Germany)

Strategic collaborations between aircraft manufacturers, additive technology providers, and advanced materials companies continue to strengthen the industry's innovation ecosystem.

Frequently Asked Questions

What is Aerospace Grade 3D Printing Additive Manufacturing?

It is the use of advanced additive manufacturing technologies and certified aerospace-grade materials to produce lightweight, high-performance components for aircraft, defense systems, and space applications.

What factors are driving market growth?

Major growth drivers include increasing demand for lightweight aircraft components, advancements in materials science, supply chain optimization, and expanding commercial space activities.

Which region dominates the market?

North America currently leads the global market due to its advanced aerospace manufacturing infrastructure and strong investment in additive manufacturing technologies.

What are the major industry challenges?

Key challenges include high equipment costs, lengthy certification processes, limited production throughput, and shortages of highly skilled technical professionals.

Get Full Report Here: https://www.24chemicalresearch.com/reports/268669/global-aerospace-grade-d-printing-additive-forecast-market-2024-2030-729

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/268669/global-aerospace-grade-d-printing-additive-forecast-market-2024-2030-729

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch